It’s 11 PM on a Sunday. Three years of monthly SIPs, not one missed. Tonight you finally sit down to calculate your returns.

₹1.8 lakh in, ₹2.3 lakh out. 27% absolute return. You feel good — until you try to compare it to an FD at 7.1% per year. One is a percentage over three years. The other is per year. They are measuring completely different things, and you realise you have been investing for three years without knowing if you actually made a good decision.

That is the problem XIRR solves.

What is XIRR?

XIRR full form is eXtended Internal Rate of Return. In simple terms, XIRR is a financial metric that measures the profitability of an investment, taking into account the time value of money. It is an annualised return on an investment where cash flows (deposits and withdrawals) happen at irregular dates.

Technically, it is a discount rate at which the Net Present Value (NPV) of all your investments and withdrawals, on their exact dates, equals zero.

Think of it as a translator. It takes your full, messy investment history across many dates and turns it into one annual percentage you can compare against anything: FD, mutual fund, stock index, PPF.

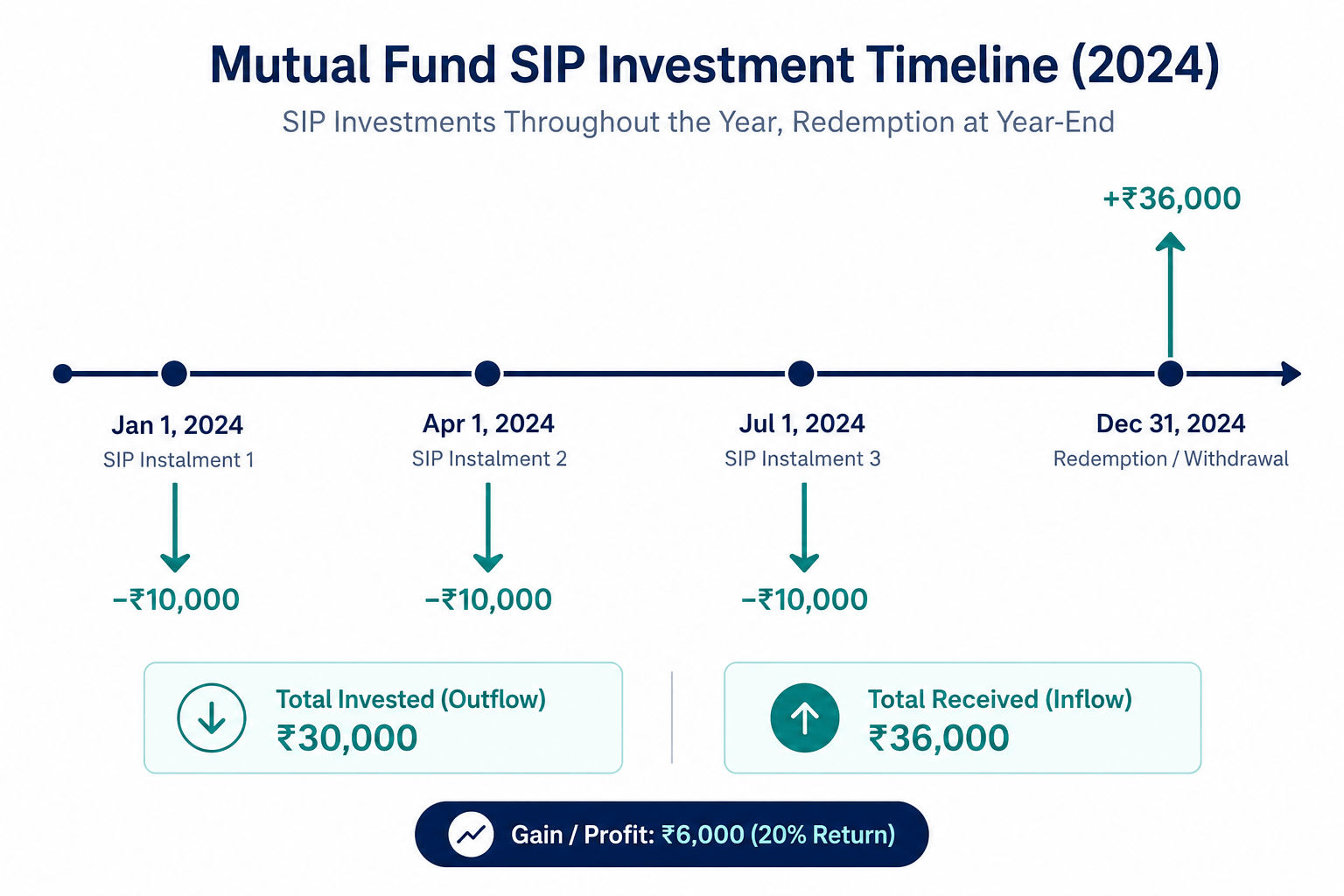

A Concrete Example

Suppose you invested in a mutual fund like this:

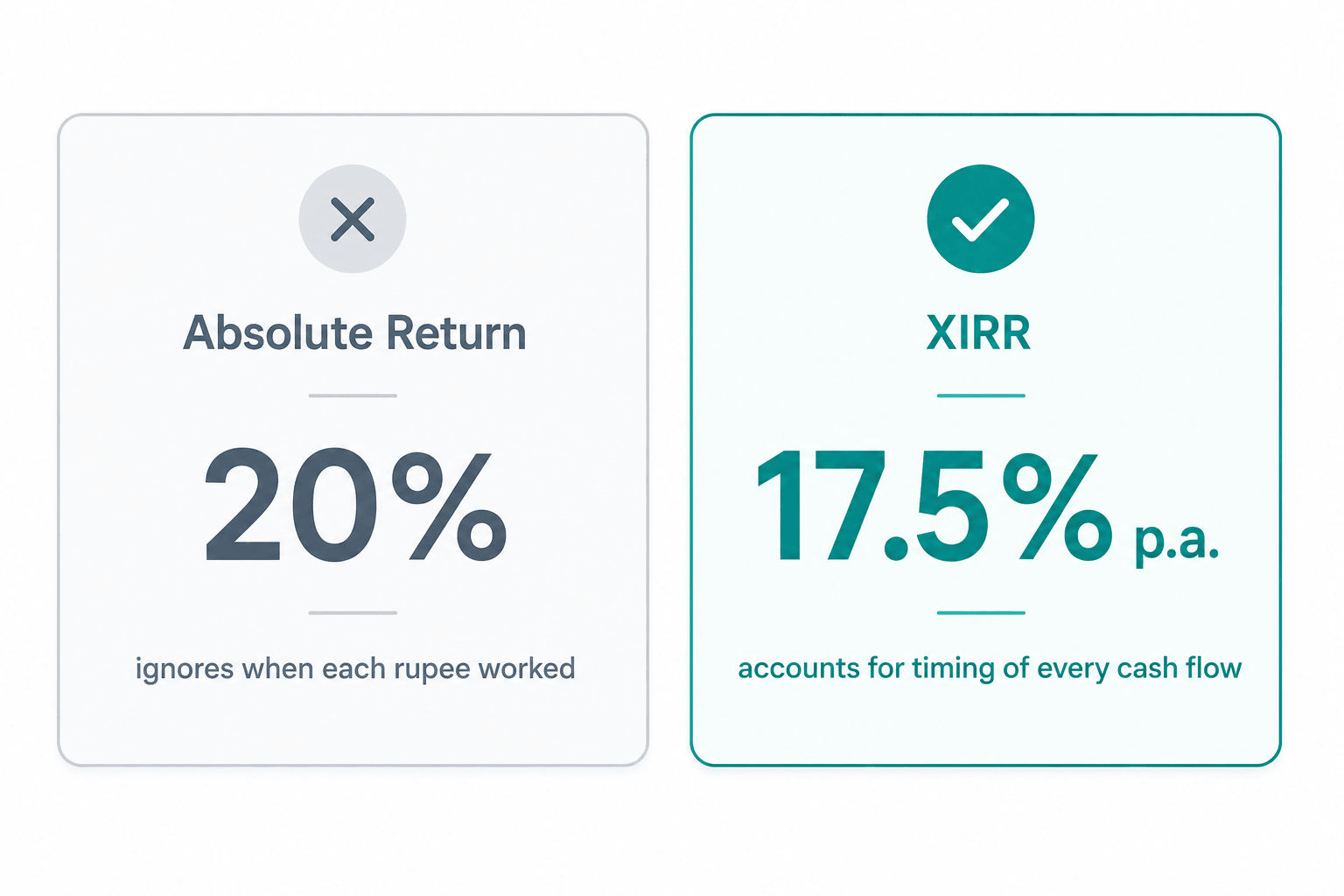

Total invested: ₹30,000. Total received: ₹36,000. Absolute return: 20%.

Simple math says 20%. But your January money worked for 12 months while your July money worked for only 6. A flat 20% ignores that entirely.

XIRR accounts for every date and every amount:

Why XIRR Matters and When to Use It

XIRR matters because timing changes results. Two portfolios can have the same total invested amount and the same current value, but wildly different outcomes depending on when the money was deployed.

Common situations where XIRR is the right metric:

- SIP investments: each instalment has a different “time in the market,” so one return number must weight cash flows by date.

- Mutual funds with multiple transactions: lump sums + SIPs + partial redemptions. Most AMCs and fund platforms already use XIRR to report annualised SIP returns.

- Stock portfolio with multiple buy/sell dates: buying in tranches, receiving dividends, partial exits. XIRR gives you the real portfolio-level return.

- Real estate: EMIs going out monthly, rental income coming in irregularly, final sale price years later. XIRR captures the full picture.

- NPS contributions: deposits across months and years with no fixed schedule.

- Business project evaluation: deciding if a capital investment paid off, given uneven inflows and outflows over time.

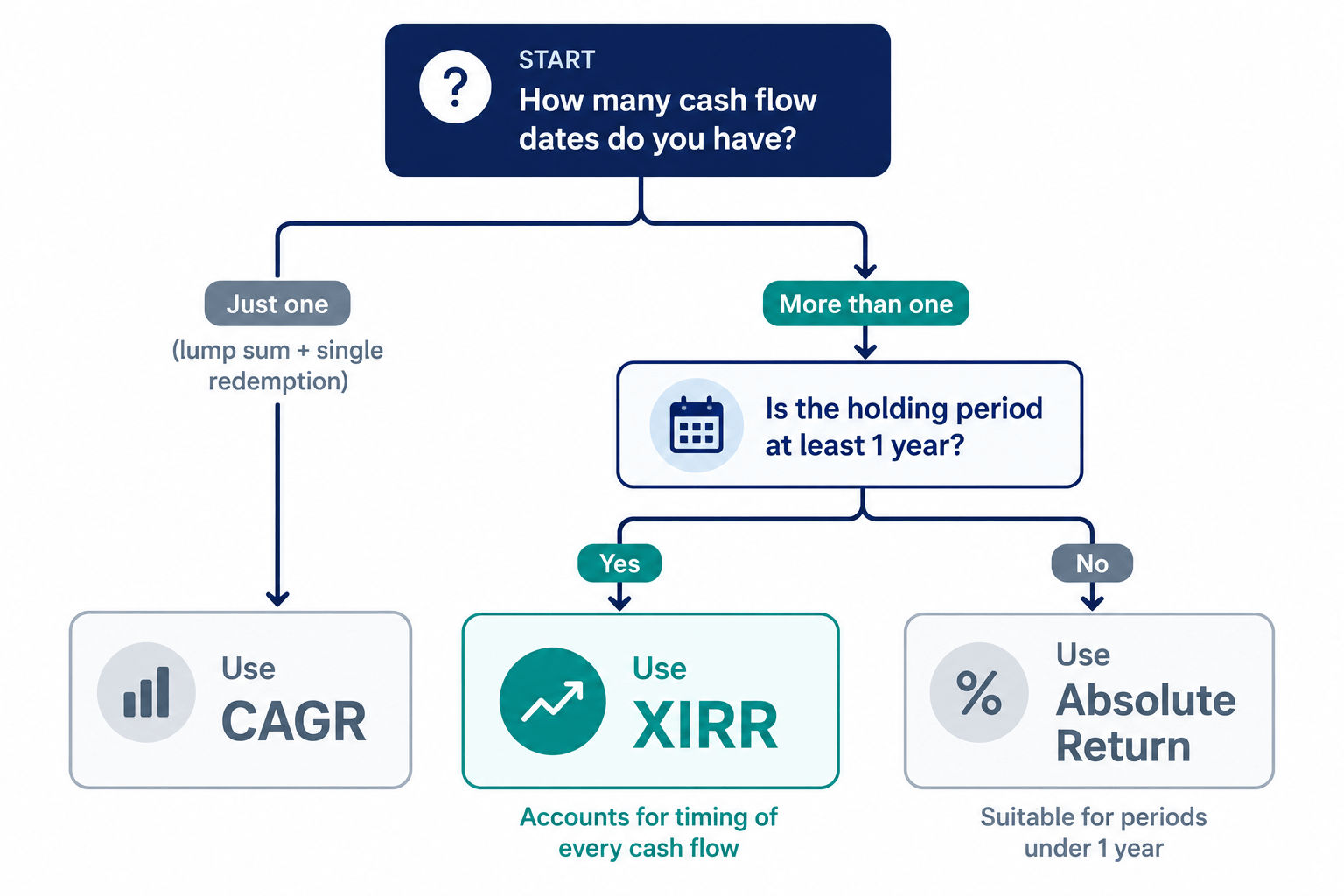

Rule of thumb: more than one cash flow date, with a holding period of at least one year? Use XIRR. Otherwise reach for CAGR or absolute return.

XIRR vs CAGR: Which One to Use?

This is the comparison most investors need before they fully trust XIRR.

| Aspect | CAGR | XIRR |

|---|---|---|

| What it measures | Annualised growth rate | Annualised return with exact transaction dates |

| Time consideration | ✓ Considers overall duration | ✓ Considers exact date of each transaction |

| Formula | (Final/Initial)^(1/years) − 1 |

Solves for NPV = 0 using Newton-Raphson |

| Number of transactions | Limited to 2 (one buy, one sell) | Works with unlimited transactions |

| Best for | Single lump sum investments | SIP, multiple transactions, real portfolios |

| Calculation complexity | Simple | Complex (needs calculator/Excel) |

| Can compare different durations? | ✓ Yes | ✓ Yes |

| Industry standard for | Mutual fund factsheets | Portfolio performance tracking |

For a single lump sum held to maturity with no intermediate transactions, XIRR and CAGR produce the same result. The moment you add a second cash flow on a different date, XIRR is the only accurate metric.

When to Avoid XIRR

- Investment period is under one year. XIRR annualises everything. A 5% gain in 2 months becomes ~35% per annum — technically correct, practically useless. Use absolute return for short-duration instruments.

- Single lump sum, single redemption. CAGR is built for exactly this. Simpler, equally accurate, less confusing.

- Fixed-return instruments like FDs, PPF, or RDs. You already know the interest rate.

- Short holding period with many transactions. High-frequency scenarios produce XIRR values that are mathematically valid but lose interpretive meaning.

How to Calculate XIRR

There are three ways to calculate XIRR:

1. Excel or Google Sheets

The practical choice for most people. Both have a native XIRR function that handles the underlying iteration automatically.

=XIRR(values, dates, [guess])

values = { -10000, -10000, -10000, 36000 }

dates = { 01/01/24, 01/04/24, 01/07/24, 31/12/24 }

=XIRR(A2:A5, B2:B5) → ~17.5%

Steps:

- List all cash flows in one column — investments as negative numbers, withdrawals as positive.

- List the corresponding dates in the adjacent column.

- Run

=XIRR(values_range, dates_range)in an empty cell.

Watch out for: Excel expects at least one negative and one positive cash flow, with dates in chronological order. A #NUM! error almost always means wrong sign convention — check that investments are negative before anything else.

2. Online XIRR Calculator

Spreadsheets work, but they require setup every time: formatting columns, getting sign conventions right, dealing with date formats. For most investors who want a quick, accurate answer, an online calculator is the faster path.

Our Online XIRR Calculator handles the heavy lifting:

- Raw copy-paste — no reformatting needed

- Bulk import — add dozens of transactions in one go

- CSV import — export directly from Zerodha, Groww, or any AMC and upload

- Instant result — no formulas, no column setup, no sign-convention errors

If you have a mutual fund SIP running for more than a year and want your real annualised return in under a minute, that is the fastest path.

3. Manual Calculation

XIRR does not have a closed-form solution. Internally, it finds the rate r that satisfies this equation:

Σ [ CF_i / (1 + r) ^ ((d_i − d_0) / 365) ] = 0

Where:

CF_i= cash flow at period i (negative for outflows, positive for inflows)d_i= date of that cash flowd_0= date of the first cash flowr= the XIRR rate being solved for

The rate r is found by iteration using the Newton-Raphson method — making an educated guess and refining it until the equation balances. In practice this converges in 20 to 100 iterations. Understanding the mechanics once is useful. Nobody does this by hand.

Critical: investments must be entered as negative numbers (money leaving your pocket) and withdrawals as positive (money returning to you). Wrong sign convention produces a #NUM! error or a nonsensical result.

Bottom Line

The investor staring at 27% absolute returns was not wrong to feel proud. Three years of discipline is genuinely hard. But they were flying blind — no idea if they beat an FD, matched inflation, or lagged the index they tracked.

XIRR converts that ambiguity into one honest number. For SIPs and most real-world mutual fund portfolios, it is the only return metric that reflects what actually happened to your money. Once you understand why timing matters, the number becomes far easier to trust — and far harder to misread.